Top Brokerages 2022

Jump to winners | Jump to methodology

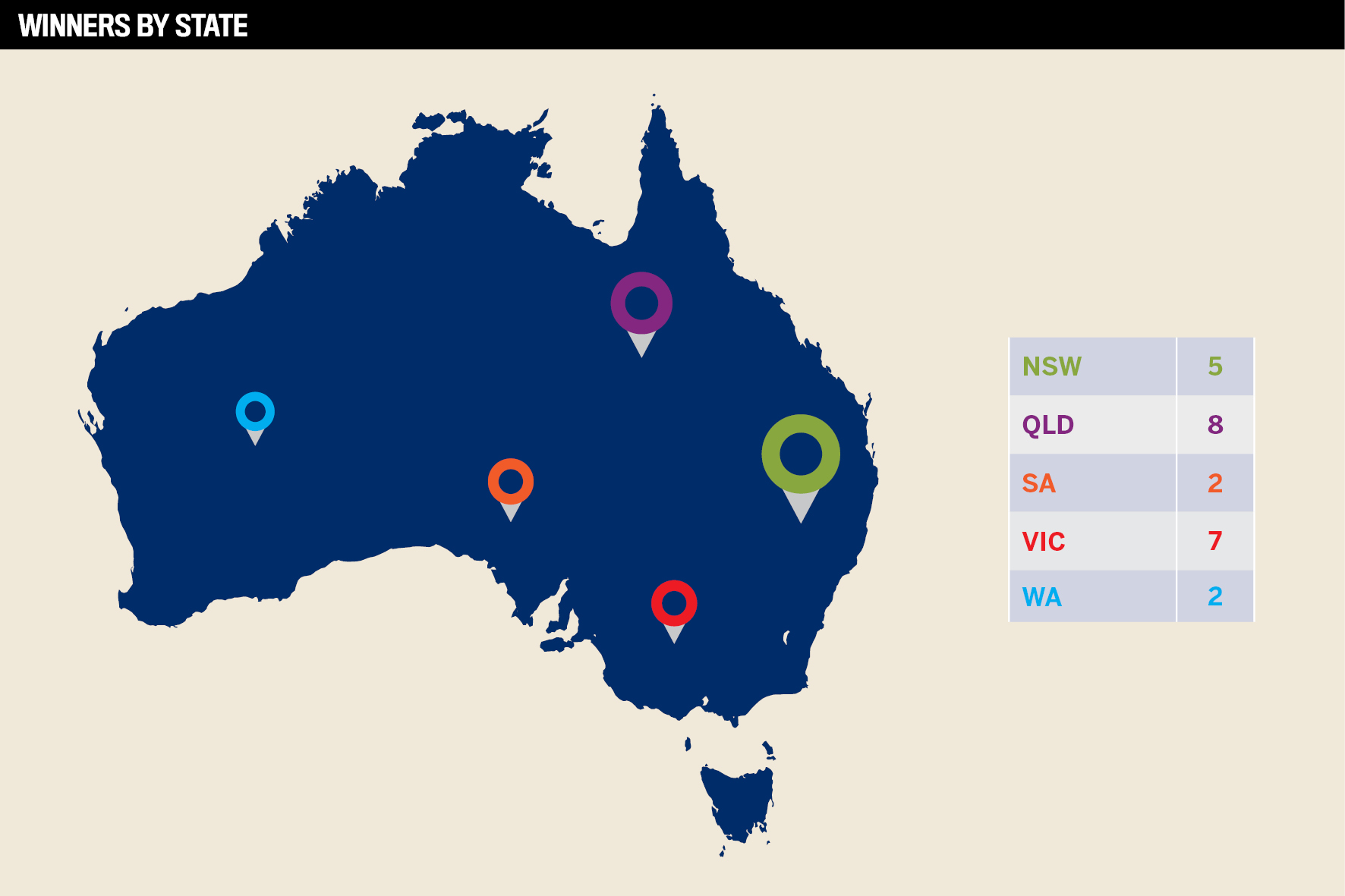

Big business brokers

Insurance broking is huge business. Intermediaries, such as brokers, placed approximately 55% of the $57.5bn GWP in the year to December 2021, according to the Australian Prudential Regulation Authority.

So not only are they doing mega numbers, Insurance Business’s Top Brokerages in 2022 have distinguished themselves by doing it professionally and effectively. It’s not an easy industry to rise above the rest. Statistics from the Australian Financial Complaints Authority showed 4,762 complaints in the last six months of 2021; however, only 29 (0.6%) of those were against brokers.

Insurance Advisernet is one of the largest general insurance businesses in Australia and New Zealand. Managing director Shaun Standfield offered his expert view of the sector, “As brokers, we need to do more to promote what we do because we don’t just place insurance, we actually advise on risk management, claims advocacy and actually support our clients with information that helps to make sure they get the right insurance coverages. I think all brokers should be proud of that.”

After reviewing impressive growth rates for clients, policies and revenue, Insurance Business gave the 2022 IB Top Brokerages awards to two dozen brokerages.

“The low unemployment rate hides the grim reality that too many Australians are still locked out of the jobs market with no way back in”

Jim Chalmers, Government of Australia

What differentiates the winners

One winner, ARMA Insurance Brokers Hunter Valley, based in Maitland in New South Wales, is doing what it needs to succeed. In addition to chalking up impressive growth figures, the company has made great advances in providing an attractive work-life balance for its employees by recently going back to a four-day week.

According to the book The 4-Day Week (2020) by Andrew Barnes, one company was able to increase employee productivity by 25% in 80% of the time by working four days a week. With this arrangement, 78% of employees are happier and less stressed and 63% of companies find it easier to attract talent, according to 4DayWeekGlobal.

But that’s not all they’ve done though to earn their Top Brokerage status. “We just never shifted from the values and the culture, and the mission and vision of our business,” says ARMA Hunter Valley’s managing director Amanda Morris. “We just kept coming back to that in the last two years and staying grounded – keeping that consistent level of customer service and ‘bubbling’ our business so that the outside influences of the world didn’t have much of an impact on us – has been the reason why we’ve grown the last two years consistently.

“We’ve got a few battle scars, but we’re a lot stronger and better than a lot of other businesses. I attribute that to the attention we spend on our employees’ mental health and the experience of the client. We do a lot of automation prior to renewal. We start 10 to 12 weeks out and nurture our clients through, so we’ve got that relationship and rapport that’s enabled us to have hard conversations, and I think that’s probably been our big point of difference. We’re very old school. We’re face-to-face brokers. We answer our phone calls. We are good to our word, and I think society is looking for that now.”

Paul Daniele, director of fellow winner Prasidium Trade Credit Insurance, echoes that perspective and notes that if employees are happy, results take care of themselves. In addition to impressive growth figures, Prasidium has achieved a more than 95% customer retention rate.

“We have a very flat structure,” says Daniele. “The owners and the directors of the business are equally as hands-on as everyone else. In regard to how we’ve seen the revenue grow, there’s been a combination of factors. Yes, with a harder market, we are seeing higher premiums. Our retention rate has been market leading, so we’ve sort of ridden the wave of that.

“It’s been the high retention rate, it’s been the referral channels, which has developed new opportunities coming through, and the referral channels are the GI brokers and the banks especially. The third one is diversifying our income streams and bringing on some other new products to generate additional income. And, lastly, we have a really strong federal program with our existing customers.”

“We have a very flat structure. The owners and the directors of the business are equally as hands-on as everyone else”

Paul Daniele, Prasidium Trade Credit Insurance

Not enough brokers

One challenge confronting the broking industry is the lack of staff to realise its full growth potential. With unemployment at a meagre 3.4%, some insurance brokerages are encouraging the government to open more migration channels.

Some are not fond of the idea. “The low unemployment rate hides the grim reality that too many Australians are still locked out of the jobs market with no way back in,” said Federal Treasurer Jim Chalmers in a recent article in the Financial Review. “Long-term unemployment is a tragedy with far-reaching and intergenerational consequence.”

Of the unemployed, 26% (or approximately 127,900) are long-term unemployed (those out of work for more than 52 weeks), according to Chalmers.

Daniele at Prasidium says the hard market conditions have placed a premium on adapting to market changes and proved his firm possesses the technical know-how to maintain excellent customer service.

“There’s a lot of shareholder motivations around consolidation. I think one of the drivers around a lot of these consolidations of different brokerages is that people want to make sure they’ve got the necessary skills and people in their companies to be able to manage these scenarios again. So, the last few years has really exposed some of those brokers who have become more complacent and need to sharpen up.

“Our biggest challenge is bringing new people in,” adds Daniele. “It’s really hard. The ability to employ even someone who doesn’t have experience, it’s just really hard to get the right people.”

Other than talent acquisition through consolidations, another option is to loosen migration restrictions. The government migration cap dropped to 160,000 in 2019-20, but for the first time in a decade it’s been raised to 195,000 for this financial year.

Standfield feels there’s no “simple silver bullet,” but his firm has been using bots for domestic and business insurance.

“I was looking at ways we can make our brokers lives more efficient, because ultimately, we want to take all the back-office tasks off them and ultimately have them spend more time with their customers. We’ve got a number of brokers now using offshore services based in the Philippines,” he explains.

“As brokers, we need to do more to promote what we do because we don’t just place insurance, we actually advise on risk management, claims advocacy and actually support our clients with information that helps to make sure they get the right insurance coverages”

Shaun Standfield, Insurance Advisernet

A taxing situation

In addition to migration issues, Daniele cites taxes as an extra challenge in the Australian market for brokers to contend with, especially the goods and services tax (GST) and stamp duties.

“The customers’ eyes light up when they see the GST and stamp duties,” he says. “Typically, we’re looking at additional costs of anywhere between 12% and 20% on any policy in regard to duties and costs.”

Meanwhile, in New South Wales where ARMA Hunter Valley is based, there’s a fire levy of anywhere from 38% to 40%.

“So, straight away we’re on the backfoot in this state because of that one change,” says Morris. “I don’t think our clients even realise how many levies in taxes and charges are on their insurance premiums, and it’s having a massive impact now because people just can’t afford to insure. I’ve tried to bring this to the forefront of our government, and it just seems to fall on deaf ears.”

Standfield echoes this frustration. “The people that pay insurance are disadvantaged because they’re paying for the emergency services, through their premiums and if you choose not to have insurance, you still get looked after by the emergency services,” he adds. “So, a fair way of doing it would be to perhaps put the levy or include [it] in your council rates and charges based on every property. That way, everybody’s paying for our proportion of the service.”

2. Shielded Insurance Brokers

3. Whitbread Insurance Group

4. IMC Insurance Brokers

5. McLardy McShane

6. (tie) Dunk Insurance

6. (tie) Maxton

8. GSK Insurance Brokers

10. Austbrokers Coast to Coast

11. Stewart Insurance Group

12. West Rock Insurance Brokers

13. Grace Insurance

14. National Credit Insurance (Brokers)

15. Elliott Insurance Brokers

16. ARMA Insurance Brokers Hunter Valley

17. CCM Insurance Group

18. Proinsure

19. Blynx Insurance Services

20. Prasidium Credit Insurance

21. Dixon Insurance Services

22. Stellar Insurance Brokers

23. Bell Partners Insurance

24. Clear Insurance

Insurance Business invited brokerages across the country to submit nominations for its 10th annual Top Brokerages list. To be eligible, brokerages were required to have three or more brokers and be headquartered in Australia. Brokerages were ranked on the following criteria:

• Number of clients

• Client growth

• Clients per broker

• Policies written

• Policies written per broker

• Revenue

• Revenue per broker

• Revenue per policy

• Policy revenue growth

As in previous years, each brokerage was required to supply its own details for the 2021-22 financial year. Brokerages were ranked according to each of the above criteria, and all of the rankings were then added together. Akin to a round of golf, those brokerages with the lowest overall scores achieved the highest rankings.

IB’s ranking system rewards brokerages based on business per broker rather than critical mass, which ensures that the very best brokerages are singled out, regardless of size.